Retirement Longevity

One thing that we spend a great deal of time on at our firm is retirement planning. If you have not gone through the process recently and made any updates, I suggest you consider putting it on your to-do list. Most people seem to get more motivated to take the time to do this as retirement becomes imminent. The more years in advance you can put your plan into place, the more likely you are to achieve your objectives. This additional time may allow for things like increasing contribution amounts to your 401(k) account, starting an educational funding account for your children, and reviewing your insurance policies to better achieve your goals, among other things.

My partner, Jeremy Nelson, likes to say there are usually three different phases of retirement, 1) the GoGo years, (2), the SlowGo years and (3) the NoGo years. When you stop and think about retirement, these different periods make sense. You may be thinking about some of your friends going through one of these times now. We have some clients that recently retired, sold everything, bought an RV, and are enjoying traveling the country. Another couple is enjoying occasional travel, but mostly staying close to their grandchildren. Yet another retiree is in an assisted-living home, with limited outside activities.

As you may imagine, their expenses can be vastly different. In the GoGo years, the hobbies, travel, entertainment, and other expenses may be a larger part of the budget while not so much during the latter NoGo years. During the latter years, expenses may be more health and long-term care related.

If you have not yet experienced retirement living, it may help to hear about the needs from people that deal with retirees on a frequent basis.

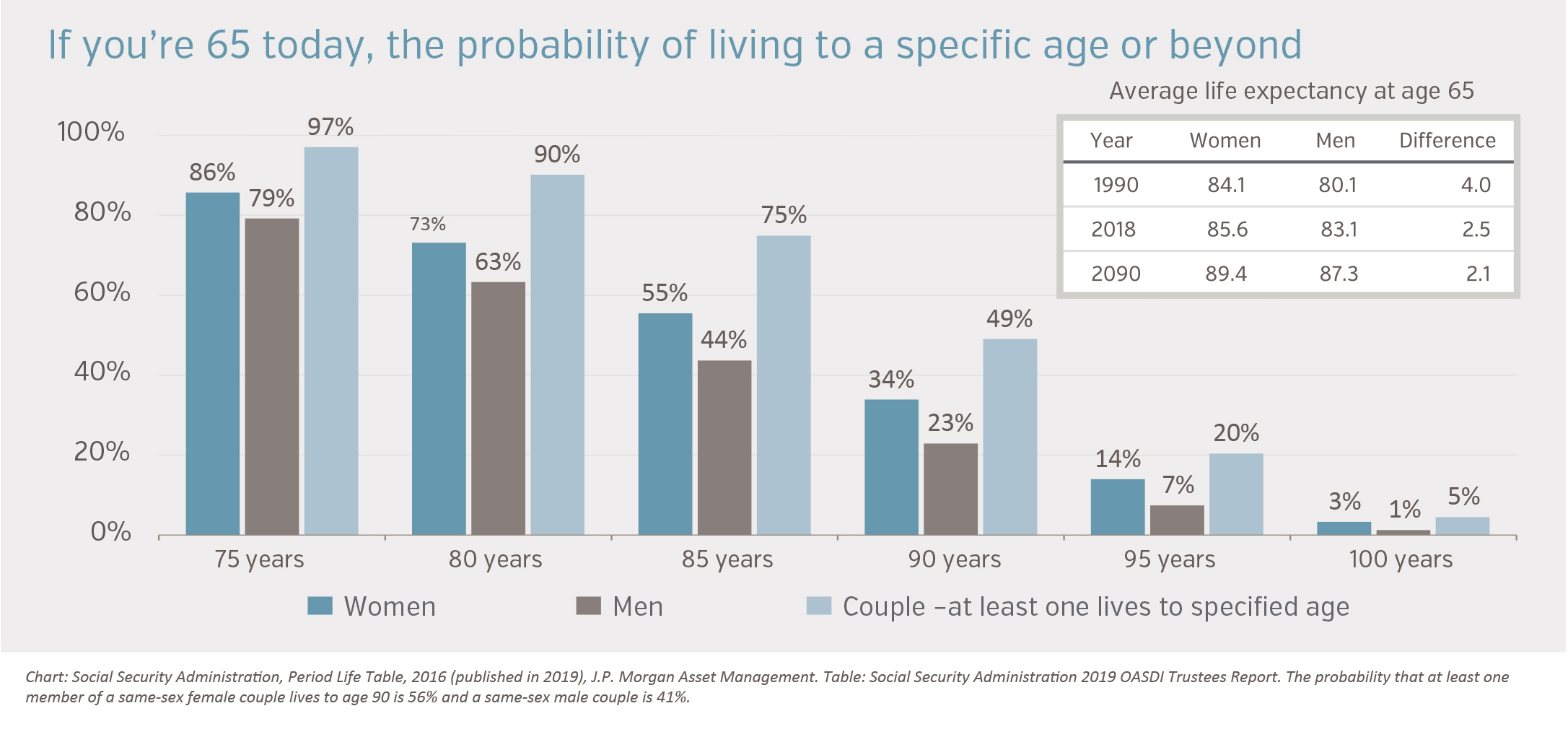

In preparation for writing this article, I Googled “hot topics” for financial planning. One of them was “planning consideration due to increased longevity”. According to the Social Security Administration, someone born in 1954 who turned 65 in 2019 is expected to live to 84.3 years, about 20 years in retirement. The World Economic Forum’s white paper, dated May 2017, said that life expectancy has been increasing rapidly, about one year for every five years. They predict that a child born in 2017 will have a life expectancy of over 100 years old. This is just a prediction, but we all know people that are living in retirement well past their mid-80’s.

In the chart on the following page, remember that average life expectancy continues to increase and is a mid-point not an end-point. Thirty years in retirement is not out of the question.

Living longer in retirement creates many challenges.

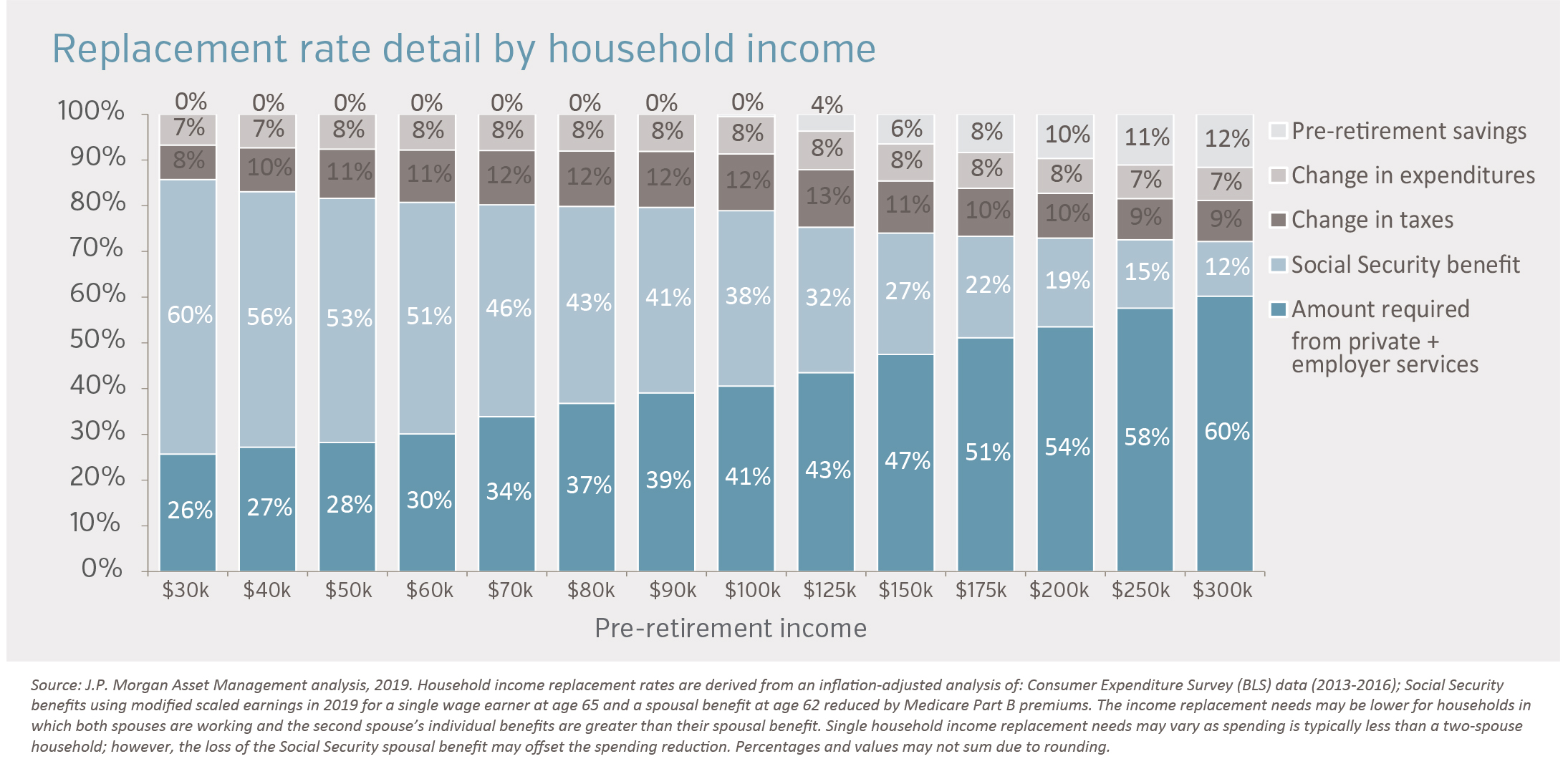

Social Security’s website tells us that it is commonly accepted that a replacement rate of roughly 70 percent is adequate income from all sources, and Social Security benefits typically account for a replacement rate of about 40 percent. Many of our clients tell us they will need upwards of 100 percent of their pre-retirement income during retirement. As we can plainly see, we need other sources to fill this gap.

During many of our meetings, we talk about finding the sweet spot in the mix of growth, income and guarantees. We believe that most investors/retirees need a well-diversified portfolio that includes assets in each of three broad categories. Everyone is different and the proportions of each are unique to the individual. For example, a company pension would fall into two categories, income and guarantees. Our objective is to produce an adequate amount of income during the estimated years in retirement.

As people get closer to retirement, they often believe they need to be very conservative with their investments. Let’s think back on the increasing likelihood of having a retirement of 20 to 30 years. If interest rates stay at these historical low levels for years to come, and your plan is only generating conservative-type returns, longevity risk may come into play.

World Economic Forum, multiple retirement system challenges are ahead. They are:

• Lack of easy access to pensions

• Long-term, low-growth environment

• Low levels of financial literacy

• Inadequate savings rates

• High degree of individual responsibility to manage pension

I will not go into each of the above challenges but there are numerous obstacles to a successful, long-term retirement. This is where timely planning comes into play, helping you identify your challenges and implement needed solutions. Do yourself a favor and set aside time to put your plan in place and have it implemented.

IS THE 60/40 PORTFOLIO DEAD?

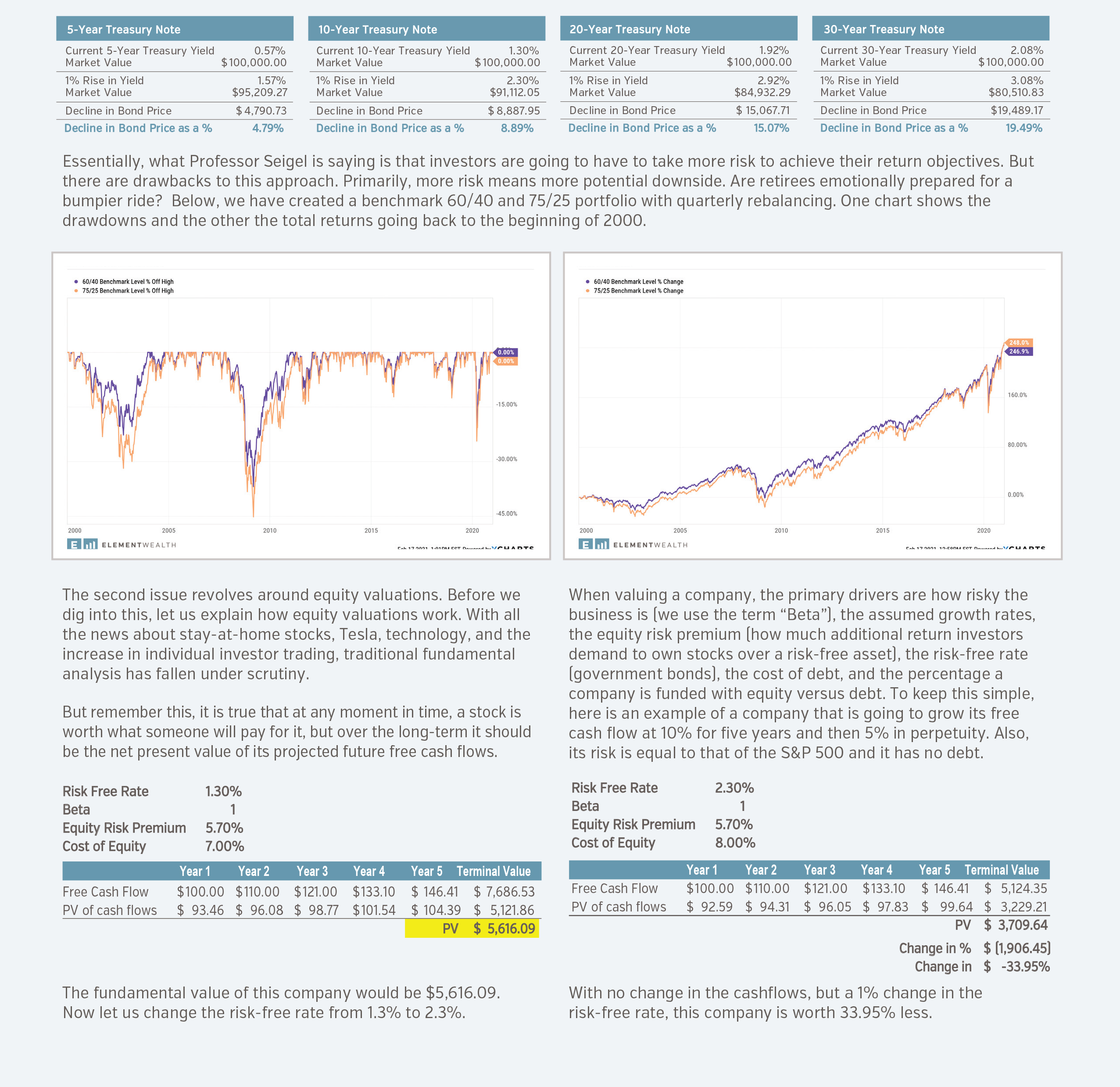

Recently, there has been a lot of talk about the death of the 60/40 portfolio. One strong voice on the subject has been Professor Jeremy Seigel of the University of Pennsylvania’s Wharton School of Business. Seigel has advocated that 75/25 is the new 60/40. With interest rates at generational lows, bond yields are not sufficient to support retirees’ income needs. According to Ned Davis Research, as of January 31, 2021, 65% of companies in the S&P 500 had dividend yields greater than the 10-Year Treasury yield.

Aside from the lack of yield on high-quality bonds, low interest rates have increased the potential for interest rate risk on balanced portfolios. When interest rates go up, bond prices go down. Below are the current Treasury yields and the impact of an instantaneous 1% increase in rates. You will notice that a 1% change impacts longer term bonds more than short-term bonds.

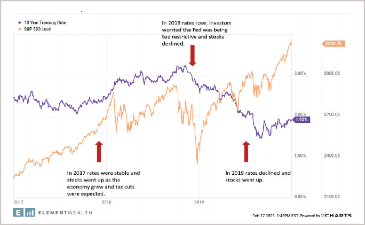

Going back to 2017 through 2019, in 2017, the 10-Year Treasury was relatively flat, tax cuts were expected, and the market went up. But as rates went up and crossed 3% in 2018, the market peaked and dropped nearly 20%. The Fed reversed course and went into an easing cycle, rates dropped, and stocks rose in 2019.

Do not worry, if interest rates rise, we do not expect the S&P 500 to drop 34%. This is an overly simplified example to illustrate that interest rates do not just affect bond prices, they affect stock prices as well!

Here is a chart that shows the S&P 500 P/E ratio versus the 10-Year Treasury rate beginning in 2011. You will notice there is a negative correlation between the two. This means that as rates go down, the P/E, or valuation, goes up. The correlation is -0.55. A perfect negative correlation is -1. So, there is more to the story than just interest rates, but it is meaningful.

So, if you are not willing to take a bumpier ride, or are concerned about rising rates and equity valuations, what should you do?

So, if you are not willing to take a bumpier ride, or are concerned about rising rates and equity valuations, what should you do?

- Remember that investing for and during retirement is a long-term proposition.

- Diversify!

- Allocations to private real estate can boost portfolio income and increase long-term return potential without adding the all the volatility of additional stock exposure.

- Multi-sector bond managers can boost income and tend to have less interest rate risk than core bond allocations.

- Shift equity allocations towards equity income. The dividends from these stocks will help boost overall portfolio income and are generally trading at much more reasonable valuations.

- Consider fixed income alternatives such as fixed or fixed indexed annuities. These allocations come with principal guarantees and can offer significantly higher crediting rates than core bonds.

- Fixed annuity rates currently provide higher crediting rates at three- and five-year terms than 10 to 30-year Treasuries.

- Fixed indexed annuities are a longer-term investment, generally 8-12 years, but offer principal protection, the ability to take withdrawals without risk to the principal, lock-in gains every 1 to 3 years, and have the potential to earn two to four times the crediting rate of core bonds.