Perspective Matters

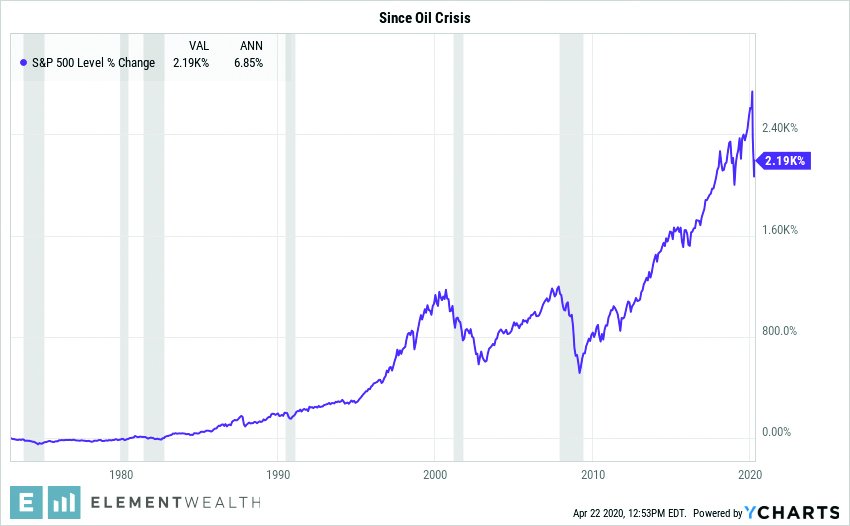

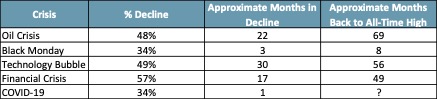

For every bull market there is a bear market. Unfortunately, this is a fact we must accept as long-term investors. Normally, a bear market ends up being a minor setback in the long-term upward trajectory for the equity market. But periodically a bear market turns into a crisis, or a crisis leads us into a severe bear market. Since the 1970s this is the 5th crisis event for the equity markets. In 1973-74 there was the Oil Crisis, 1987 had Black Monday, 2000 saw the Technology Bubble burst, and in 2008 we entered the Financial Crisis. The current COVID-19 crisis is not the first crisis we have faced, and it certainly will not be the last.

When we are in the midst of a crisis, it is critical that we take a step back and put things in perspective.

First, we must remember that over the long-term, equities produce superior returns to bonds. Since the beginning of the Oil Crisis, the S&P 500 has produced annualized returns of 6.85% without dividends. With the 10-year Treasury bond currently below 1%, the bar is low.

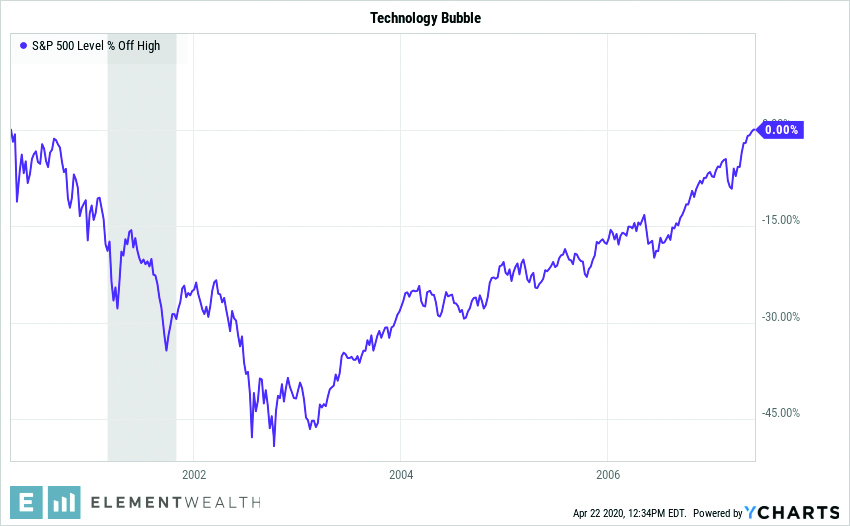

Second, we have to take a look back at other crisis events to evaluate the magnitude, duration, and time it took to recover. The Oil Crisis, Technology Bubble and Financial Crisis saw deeper and more prolonged declines, with a longer recovery time than Black Monday.

Third, we must consider the driving forces and ask:

- What is similar?

- What is different?

- What are we missing?

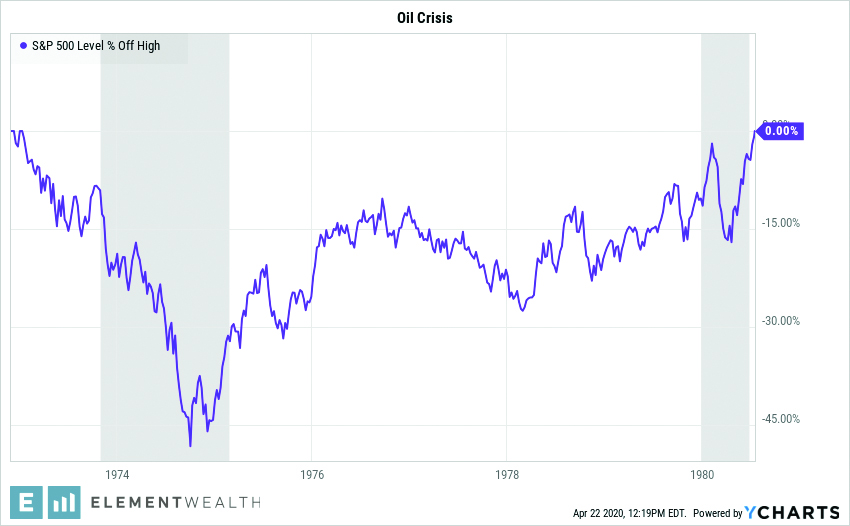

The Oil Crisis created an inflation problem, interest rates rose, and valuations on stocks plummeted. Declining stock valuations or multiple contractions held the equity market down throughout the 1970s. Aside from the fact that there was a recession, there are not a lot of parallel themes to draw from as inflation has not been a problem for decades and we have an overabundance of oil.

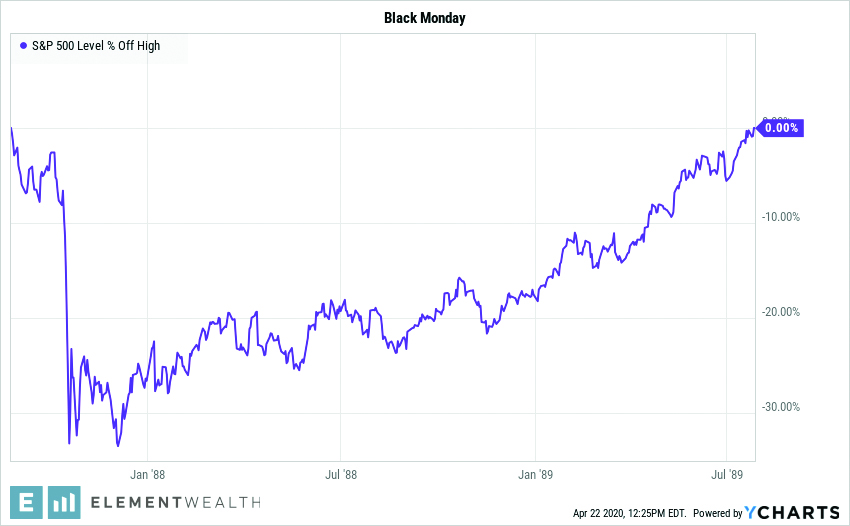

Black Monday is largely believed to have happened due to computer program-driven trading models that followed a portfolio insurance strategy. Selling started and panic set in leading to the most rapid bear market in history. Things settled down and the market recovered in approximately eight months. The rapid declines are surely a strong parallel. However, this time we do have a recession. But this recession is driven by a health crisis, that, if contained, will likely lead to a strong economic recovery in 2021. Assuming that the bottom is in and considering the brief but steep nature of the decline, as well as the damage to the economy, a recovery time slightly longer than 1987 is highly probable.

The Technology Bubble was a true stock market bubble where valuations burst. Then 9/11 hit and a recession proceeded. The only parallel to 2000 is the fact that stock valuations were elevated going into the COVID-19 crisis. However, valuations were nowhere near the levels of 2000 and somewhat justified by a much lower interest rate environment.

The Financial Crisis was created by an over-leveraged banking sector and a housing bubble. Stock valuations in 2007 were similar and we did have a recession. However, this time the banking sector is on strong footing, the recession is government mandated and not a result of speculation or structural issues, and the monetary and fiscal response has been much quicker and less partisan. Also, there is a general willingness of creditors to work with borrowers to get through the crisis. Although the magnitude of the recession will be severe, as it was during the financial crisis, the economic recovery should be quicker.

One crisis that has been omitted, purposely, is the Depression. Some have claimed that our current cycle is the beginning of a new Depression. We believe a related Depression has a very low probability of occurring due to the magnitude of the monetary and fiscal response to the crisis. However, we do believe there will be limitations on future post-crisis economic growth as government debt and deficit levels will have to be addressed.

The true unknown in all of this is the virus itself. Without a vaccine or cure, we could be susceptible to future outbreaks. We also do not know how quickly people will be willing to get back to life as we knew it. Our expected case is for the economic decline to slow and bottom in the second quarter. People will remain cautious in their activities so we will begin to slowly recover in the third quarter and fourth quarter. Assuming the virus is under control, 2021 will mark the real recovery. Our thought is the stock market is currently pricing based on this scenario.

Jeremy Nelson, Partner

Is Average Return Relevant?

Most of you probably know that the stock market, on average, returns around 10% a year. Mutual funds, variable annuities and other products tied to the stock market advertise using the average rate of return. This is a problem, but why?

The average return is a simple calculation. You add the annual returns and divide them by the number of years you’re observing. In the investment world, the simple average is a way to smooth out the effects a loss can have on a portfolio, and this has the effect of inflating return numbers.

The actual, or “real” rate of return is achieved by adding/subtracting the annual return each year, then starting each year with the new value. This is also referred to as the compound annual growth rate (CAGR).

The reason you don’t hear about this number is because it is always lower than the average.

For example, let’s say you invest $100,000. At the end of the first year you have a return of +20%, and the second year you have a return of -20%. The average return would be 0%. This is the number the industry will have you looking at, but is this relevant?

Let’s look again. An investment of $100,000, multiplied by its return of +20% equals $120,000 at the end of year one. Year 2, $120,000 multiplied by -20% equals $96,000. After the two years your actual return, or CAGR, is -4%.

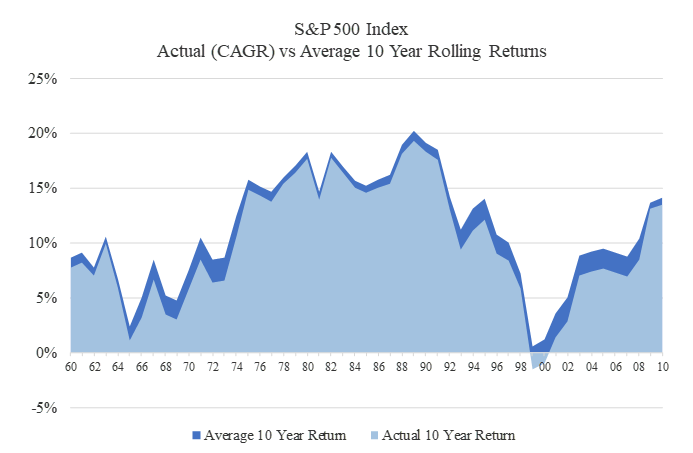

Below is a chart showing actual versus average return for the S&P 500 from 1960-2019 on a 10-year rolling basis. The average returns are represented by the dark blue “mountain” in the background, while the light blue mountain represents the actual compounded rates of return. For example, the average annual return from 1993-2002 was 11.26%, right about at the historical average we hear about. However, someone who actually invested in the S&P 500 from 1993-2002 would have only realized a CAGR of 9.39%.

How can someone have less money than when they started, when the average return was 0%? Because when you lose money, you have that much less capital in order to generate returns during the following years, and the impact of a loss has a much greater influence on your portfolio than a gain.

The point is, the “actual return” is the ONLY return that really matters. It gives you the ability to see how an investment truly performed over time.

Barry Smith

As if we didn’t have enough to worry about right now, scams related to coronavirus are on the rise. And the fraudsters are pulling out the stops. According to the Consumer Financial Protection Bureau, here are some things to take note of:

Some of the scams currently in the mix include:

- COVID-19 vaccine, cures, et – There is currently not a vaccine, nor a known cure for the virus. In addition, it cannot be removed/filtered through your air conditioning system.

- Charity scams – Are you receiving phone calls from unknown parties asking for contributions? Perform your due diligence first. Be sure to speak with a trusted contact or research the organization online to ensure the group calling you is a viable, trustworthy nonprofit. There are a variety of resources to provide detailed information.

- Disadvantaged person – Has a friend or relative called asking for money due to losing a job or being ill because of coronavirus? Do you recognize the phone number? Voice didn’t sound familiar? Call your friend or relative using the contact info you already have. Reach out to other family members and confirm that they are truly in need before sending any funds.

- Social Security benefits – If you are contacted regarding a decrease or suspension of your benefits, don’t believe it! If you do receive such communication, be sure to reach out to the Social Security Administration for assistance.

Most importantly – remember to keep your personal information to yourself. Don’t share your Social Security number, date of birth, account numbers, etc. with anyone you don’t know. If you’re not sure about the situation, discuss it with a trusted relative or friend.

For more information regarding protecting yourself, follow this link to the website for the Consumer Financial Protection Bureau ( https://www.consumerfinance.gov/about-us/blog/beware-coronavirus-related-scams/).

The Merits of Monitoring

I noticed a headline recently that was titled “The Merits of Mentoring,” and at first, I thought it read “The Merits of Monitoring,” which I have always encouraged clients to do. I believe that your success probability is greater if you have a written financial plan and continue monitoring your progress over the years. I consider the relationship we have with a client as a partnership. Like most healthy and productive partnerships, all partners need to be actively engaged in the endeavor.

This process takes some time in the beginning and periodically along the way, but one should be rewarded in numerous ways while approaching and during the retirement years. The financial planning process is mainly utilizing information that we know today. So, as the saying goes, the plan is only as accurate as the information going into it. While this fact may be somewhat accurate and discouraging, having a plan for most anything will improve the probability of success.

The monitoring piece of the puzzle helps reaffirm that the investor is still on track and helps identify needed updates and adjustments. One thing that can derail an investor is emotions. Some have a natural tendency to become more aggressive in good markets and more conservative in downturns. Greed and fear seem to be the top two emotions that come into play. As we have seen in recent months and years, the market swings can be fast and furious. If our strategies are not already aligned appropriately with an investor’s needs, it may be too late to make adjustments before markets move. We need to be in position to take advantage of market opportunities as well as maintain predetermined risk levels throughout these market corrections.

As we build a financial plan, we like to incorporate three pieces: income, guarantees and growth (with optionality). For example, if the set amount for income sources like Social Security, pensions and annuity benefits are adequate, we may reduce the risk in the growth and income components. We know everyone is not fortunate enough to have enough income generated by the guaranteed portion, so we may dial up the risk we allocate in the other areas. Each person is different, so our overall allocation needs to be customized. I was reading in “A Wealth of Common Sense,” by Ben Carlson, CFA, that every portfolio should be built with the understanding that bear markets are a fact of life when investing in risk assets. The conventional measurement of a bear market is a 20% decline. Carlson’s research counts 24 bear markets since 1928, one every 3-4 years, with the average fall from grace being a 33% drop, lasting just shy of a year from peak to trough.

Monitoring the plan helps keep the investor up to speed with one of the most important aspects of their life, other than, maybe faith and family. The stress level can be greatly reduced by having taken the time out to periodically check in with us, to get refreshed and updated on the path and goals you have set in place. We encourage you to call us if we may help you initiate or update your plan.

Danny Williams